When an investor sells their shares in a fossil fuel company to buy into greener energy, they often celebrate a “cleaner” portfolio. However, according to Mattias Gunnemyr, researcher at the Financial Ethics group at the University of Gothenburg, this approach — often based on attributional metrics — often overestimates investors’ causal impact. These metrics, he argues, are a form of financial association that can lead to misleading conclusions about real-world climate impact.

In a recent research seminar for the Sustainable Finance Lab, titled The Climate Impact of Investments, Gunnemyr argued that to truly understand the ethics of finance, we must move beyond “counting” emissions to determine climate impact and start measuring causal influence — did your action contribute to climate change?

Current climate reporting frameworks, such as the Greenhouse Gas Protocol and ESG metrics, rely on attributional metrics. Emissions are allocated in proportion to ownership. They signal a climate impact of divesting that might “look good on paper” but fail to recognize the effects through different ‘impact channels’, such as engagement.

A consistent, socially responsible decision-maker, Gunnemyr suggests, should not just be concerned with their value chain (what they own), but with their consequential responsibility (the actual real-world impacts triggered by their actions). In other words, true responsibility requires measuring leverage, not just association.

His interest in this problem grew out of earlier philosophical work. During his PhD at Lund University, Gunnemyr studied collective harm — situations in which many individuals contribute to large-scale problems like climate change.

“There are many accounts,” he explains, “like Kantians saying we shouldn’t drive to work because it’s unfair to those who reduce emissions, but the solution I’ve worked on is that this is a question of causation.” Even if you do not single-handedly make a decisive difference, you may still causally contribute to the outcome — much like taking a long shower during a water shortage.

Philosophical Hurdles: Overdetermination and Preemption

Some people suggest that causal influence and consequential responsibility should be measured by considering the difference an action makes. However, Gunnemyr highlights that this way of measuring impact faces challenges.

One is overdetermination, which Gunnemyr illustrated with the “11–0 vote:” If a resolution passes unanimously, any single vote seems unnecessary. Likewise, if one investor divests, another typically steps in.

The other is preemption: If two people throw rocks at a bottle and one hits first, the second rock becomes irrelevant, but the first still counts as a cause to it breaking. In markets, actions may remain causally relevant even if the outcome would likely have occurred anyway.

“When you try to measure the impact in stock markets, these problems of overdetermination and preemption are plentiful,” Gunnemyr explained.

From All-or-Nothing to Degrees of Causation

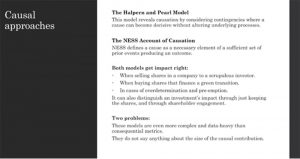

To navigate these challenges, Gunnemyr utilizes theories of causation, including the Halpern and Pearl Model and the NESS account of causation (Necessary Element of a Sufficient Set). Under the former framework, you are a cause if your action would have changed the outcome in a relevant contingency (e.g. if the policy had won by one vote). In the latter, you are a cause if your action was a necessary part of a group of conditions that, together, were enough to produce the result.

“If you go for a drive, you contribute to climate change even if you don’t make the difference,” he says.

Applied to investing, these theories and others that account for degrees of causal contribution, reframe the divestment debate. A shareholder who remains invested and votes for climate resolutions may form part of the sufficient set that produces corporate change. Even if a vote passes comfortably, each “yes” vote contributes causally. Divesting, by contrast, often removes the investor’s only channel of influence.

But engagement depends on leverage. “Some shares have very small voting rights,” Gunnemyr points out. Investors seeking real impact must consider governance structures and voting power — not just ownership.

Slide by Mattias Gunnemyr for SFL seminar, 2026.

Practical Limits and Moral Clarity

Gunnemyr acknowledges that these causal theories require projecting how actions influence future emissions — an exercise that depends on substantial data and often rests on uncertain assumptions.

As a result, applying such theories in practice may be unfeasible for many investors. In those cases, he recommends focusing on strategies that have a demonstrated likelihood of producing positive climate impacts, such as enabling high-impact companies to grow, or working towards the transition of fossil-fuel-intensive companies.

Additionally, because attributional metrics are deeply embedded in regulation, reform may need to be gradual — retaining attributional carbon footprinting while cross-checking it against consequential analysis to avoid misleading signals.

The implications extend beyond finance. Many people experience what Gunnemyr calls “moral anxiety” in everyday consumption decisions such as buying non-organic milk. However, once impacts are quantified, isolated consumer choices often prove marginal.

“Quantifying the likely impacts of our choices can also help identify the actions that do matter more”, Gunnemyr says. “While it is not always obvious what those are, engaging politically and acting together with others would probably rate quite high”.

Beyond Footprints

Gunnemyr’s ongoing research continues to examine how investors causally contribute to corporate change and how trade-offs. such as between climate and biodiversity, are measured.

“People think building with timber is always good for the climate, but it can harm biodiversity through logging. Currently, those reports are all attributional, and it’s strange how they weigh those impacts”, he says.

Across these questions, one principle remains central: The ethical issue is not merely what we are associated with, but what we are helping to bring about.

Below are Mattias Gunnemyr’s recent publications and recommended readings to delve further into the topic:

Gunnemyr, M. and Brülde, B. (2026) “From footprints to impact and back again: Calculating corporate climate contributions,” Politics, Philosophy & Economics, p. 1470594X251414938. Available at: https://doi.org/10.1177/1470594X251414938.

Gunnemyr, M. (2025) “Estimating degrees of causal contribution,” Synthese, 206(3), p. 166. Available at: https://doi.org/10.1007/s11229-025-05142-z.

Recommendations to get into the topic:

Braham, M., van Hees, M. Degrees of Causation. Erkenn 71, 323–344 (2009). https://doi.org/10.1007/s10670-009-9184-8

Weidema, B.P. et al. (2018) “Attributional or consequential Life Cycle Assessment: A matter of social responsibility,” Journal of Cleaner Production, 174, pp. 305–314. Available at: https://doi.org/10.1016/j.jclepro.2017.10.340.